Cause or Consequence?

The startup economy is suffering. Who's to blame?

The latest data on early-stage venture deals in 2023 highlights a harsh reality for a startup ecosystem. Q3 2023 data from Carta shows that the Seed and Series A funding round count is down 50% compared to Q3 2021.

However, when we look at both sides of the equation — founders AND funding — the startup world’s problem isn’t one-sided or isolated to decreased funding activity.

This edition of Human Capitalist examines the latest data on new founders in 2023, the relationship to early-stage funding, and the consequences likely to carry over to 2024. Explore the data on the health of the startup ecosystem and questions including:

a) Is the startup ecosystem in a downward spiral?

b) Who's job is it to be risk takers?

c) Who is still founding companies in 2023?

Explore the relationship between new founders and early-stage venture funding below. Plus, as always, read to the bottom for three quick hits of the best human capital insights and the opportunity to submit your own human capital questions.

Why are there fewer founders?

The number of new founder roles in 2023 is down 47% versus the previous 5-year average. A decrease that mirrors the drop in early-stage funding activity.

Regardless of which side you view as the independent variable, the correlated relationship between new founders and early-stage funding highlights an ecosystem that is in a downward spiral with no clear path out.

2023’s dramatic drop in founders and funding, and the predicted continuation of the trend in 2024, raise concerns across the early-stage community and the broader economy.

Whether you think the slowdown is driven by a lack of funding or a lack of founders — you're right. Explore the factors slowing the early-stage ecosystem:

1. Gun-shy investors

Following an extended period of exuberant investments and inflated valuations, VCs are demonstrating increased risk aversion and are returning to a more measured deployment of capital.

This recalibration results in fewer early-stage investments and a higher threshold for funding, with VCs seeking greater proof of concept and a clearer path to profitability before committing funds.

2. Unfavorable conditions for founders

Despite a slowdown in new founders, it is hard to imagine that there are fewer ideas for new companies in 2023 than there were in 2021. The reality is that the startup world is looking for a new equilibrium and founders are increasingly faced with the reality that outside capital is harder to come by and that the risks that they have to take may be a bit beyond their means.

3. Shifting macro conditions

The decline in new founders is a symptom of multiple economic factors. We’ve ended two ZIRP (zero-interest-rate policy) periods that spanned 10 of the last 15 years. Access to capital is tightening, interest rates are climbing, and the cost of borrowing is increasing. Rising inflation rates, predicted recession, and market instability all encourage a more conservative approach.

4. Layoffs

The companies that have traditionally been a bastion of startup activity, have undergone rounds of layoffs. While this could potentially increase the pool of prospective founders, it also fosters a climate of risk aversion. Potential founders, witnessing market volatility, may opt for the relative safety of their current employment over the precarious journey of founding a startup.

5. More startup failures

The increased rate of startup failures in 2023 has also contributed to a more cautious atmosphere. Each failure serves as a cautionary tale for both founders and investors.

“You go first…”

Who's job is it to be a risk taker?

While both funders and founders may be right to look at the current state of the startup ecosystem through less than rose-colored lenses, the two sides are co-dependents.

The ecosystem thrives when both sides are willing to take risks with founders challenging the status quo and VCs placing bets on new ideas.

The professional VC class is paid to take risks when backing the next generation of world-changing, return-generating companies. Entrepreneurs are rewarded for taking risks to innovate despite the high rate of failure.

From the funding side, VCs need to start writing checks (despite a changing comfort with risk) in order to facilitate an arena where entrepreneurs are supported and encouraged to innovate.

Who is going to back the bold?

Given everything highlighted above and the least favorable early-stage conditions in years, I tip my hat to the founder Class of 2023 — those taking risks in this climate.

What drives someone to start a company in the toughest early-stage climate in years?

Do they have a truly innovative idea?

Are they more dedicated and gritty?

Are they more boneheaded?

VCs looking to deploy capital into the founders who fit into bullets 1 and 2 will face increased competition for deals. It will be more important than ever for investors to improve and scale their deal sourcing and diligence processes.

Three quick hits

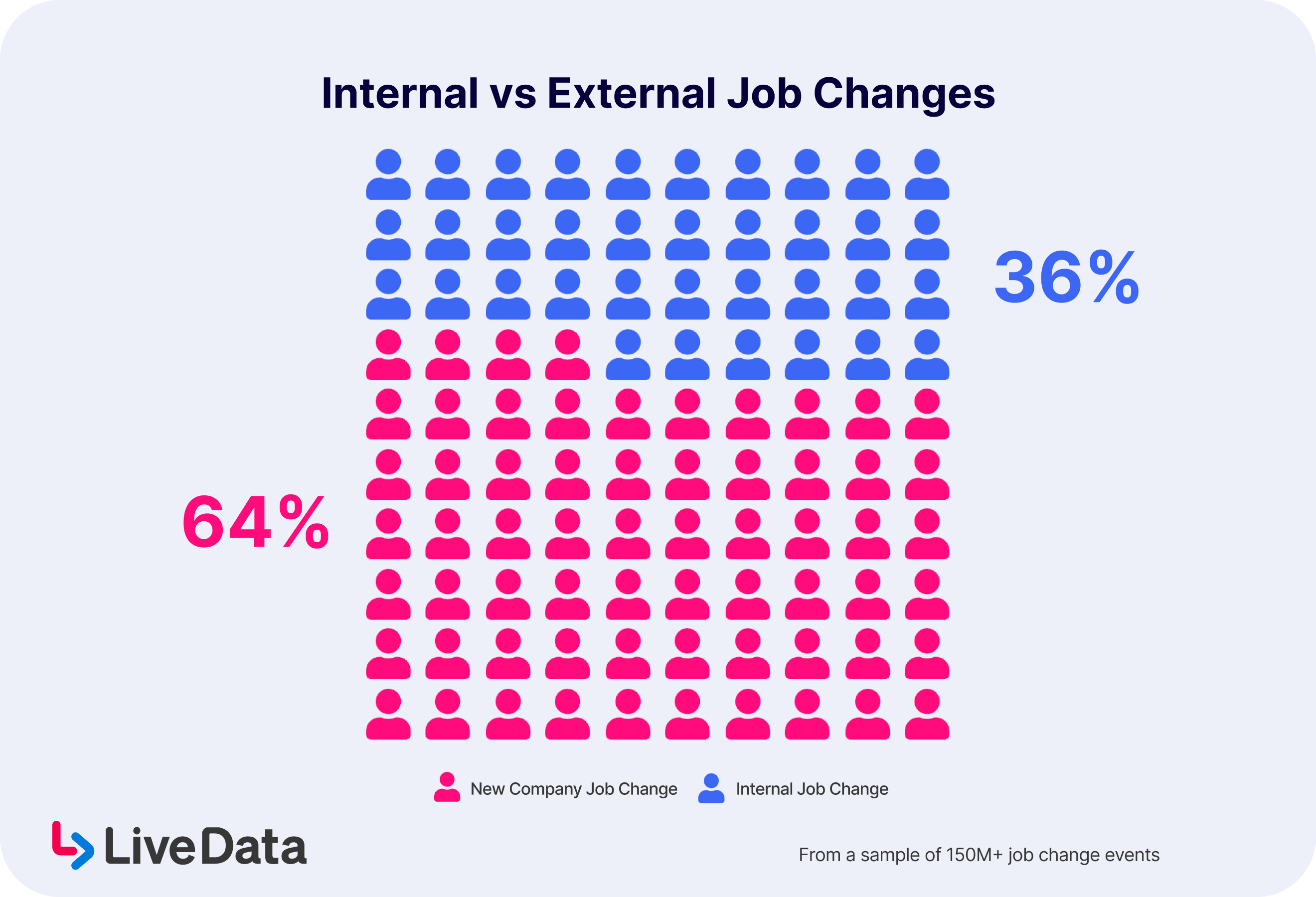

1) To stay or to leave?

Millions of people have a job change event every year. Almost twice as many people leave a company (voluntarily or involuntarily) than get promoted.

Explore the analysis of 150M+ job change events here.

2) Where are the high-tech jobs?

The Bay Area is dead, long live the Bay Area.

The SF Bay Area remains the hotbed for high-tech and has almost 2x more new jobs (per 100k residents) at high-tech companies than any other metro in 2023.

Read more about the geographical distribution of new jobs in high-tech here.

3) Do you need a technical founder or co-founder?

Do you still need a technical founding team to raise from VCs?

The data shows that 66% of unicorn startups have a founder or co-founder with a technical background. Somewhat shockingly, this percentage has been dropping for new VC-backed startups for the last 5 years.

Join the technical versus non-technical founder debate here.

What questions would you ask?

To put context around the “big numbers” of real-time human capital and job change data — specifically, 30k+ daily changes across 90M+ people at 4M+ companies — I started asking questions of our data.

For every question, there are answers, insights, and… more questions.

I’m constantly thinking about the next batch of questions and insights to dig into. If there is a human capital data question you’re interested in exploring, leave a comment below or reach out directly via LinkedIn.